Finance Department

Finance

Our Commitment:

To deliver quality financial services for City of Kwekwe. Our commitment is to provide support services in a professional and efficient manner, to achieve high levels of productivity and customer satisfaction.

Legal Basis

| Description | Act of Parliamnet | Section in the Act |

|---|---|---|

|

Rates |

Urban Council's Act |

S219 |

|

Service Charges |

Urban Council’s Act Water Act 20:22 Environmental Management Act 20:17 |

S168, 172, 179, 183, 217; 2nd Schedule para 23. S55 (d) |

|

Control & Management of Public Resources |

Public Finance Management Act Part 2 |

S6-27 |

|

|

Statutory Instrument 144 of 2019 (Treasury Instructions) |

|

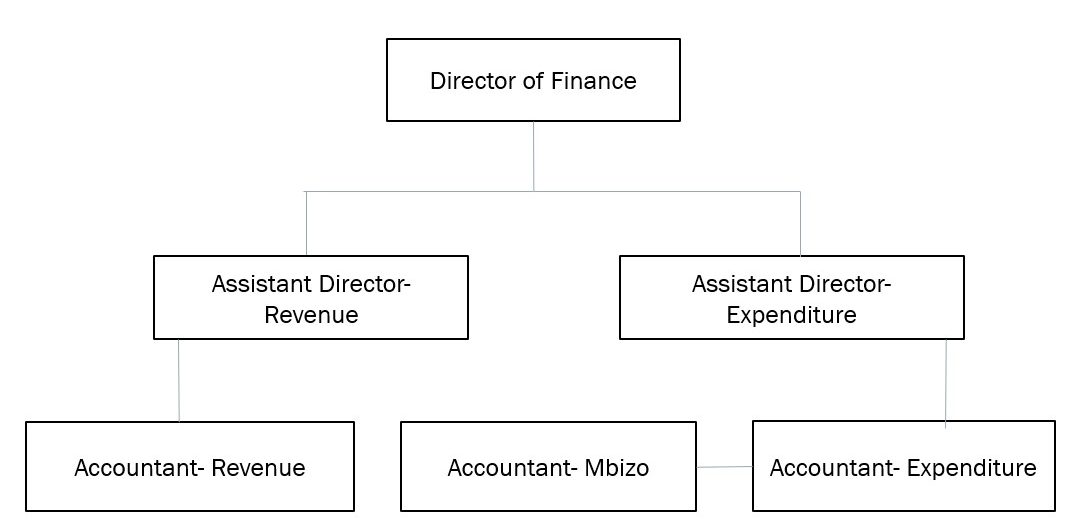

Organogram

Structure of the Finance Department

Sections under Revenue

Utility Billing and Accounts Receivable

Cashiering

Credit Control

I.T

Risk Management

Sections under expenditure

Budget Reporting and Control

Stores

Accounts Payable

Payroll

Investments

Asset Management and Insurance

KEY FUNCTIONS OF THE FINANCE DEPARTMENT

- FINANCIAL REPORTING

- REVENUE COLLECTION

- INFORMATION TECHNOLOGY AND E-GOVERNANCE

- BUDGETING AND BUDGETARY CONTROL

- FINANCIAL MANAGEMENT

2) REVENUE COLLECTION

Revenue Collection: Is collecting current and outstanding financial obligations or dues from rate payers.

Objective: To ensure that all revenues, rates, water, service charges, rentals and any other charges due to council are collected timeously in a cost effective manner.

Revenue Collection involves:

- Timely production of monthly and quarterly statements

- Debt collection blitz- Water Disconnections

- Sending bulk sms reminders

- Awareness Campaigns

- Citizen Engagements

- Issuing of Rates Clearance Certificates after requesting for upfront payments

3) BUDGETING & BUDGETARY CONTROL

Budgeting & Budgetary Control: It’s a comprehensive and coordinated plan, expressed in financial terms for the operations and resources of the council for a specific period (one year).

Objective: Increased efficient use of council resources.

Budgeting & Budgetary Control involves:

- Assisting council departments with budgetary control

- Analysing budget performance monthly

- Production of quarterly budget performance reports

- Advising council on Budget performance

- Facilitating the budget process

- Production of the budget and submission by due date

5) FINANCIAL MANAGEMENT

Financial Management: It’s the efficient and effective management of funds in such a manner as to accomplish the objectives of the organization.

It is the planning, organization, controlling and monitoring of financial resources of an organization.

Objectives: Proper mobilization and utilization of council resources.

: Maintain adequate cash flows.

:To avoid wastage and misuse of finances (financial discipline)

Financial Management involves:

- Budget Variance Analysis

- Managing scarce resources

- Maintaining Cash Flow management systems

- Revenue and Payments Cycle Management

1) FINANCIAL REPORTING

Financial Reporting: Is the process of documenting and communicating financial activities and performance over specific time periods. UCA section 286 and PFMA Sections 32-38

Objective: To provide information on the revenue, expenses, debt load and ability of Council to meet its short term and long term financial obligations.

Financial Reporting involves:

- Preparation of Financial Statements

- Preparation of Monthly Reports

- Statutory Audit of Financial Statements

Preparation of Monthly Report (Treasurers Report)

The importance of the report is:

- To analyze monthly income and expenditures

- To analyze budgetary information (Actual vs Budget)

- To report on council receivables and payables

- To analyze cash flow position

- Ratio Analysis

4) INFORMATION TECHNOLOGY & E-GOVERNANCE

Information Technology: Is the use of computers to create, process, store, retrieve and exchange all kinds of electronic data and information.

E-Governance: Is the use ICT to provide and facilitate services, exchange of information and integration of systems.

Objectives:

Information Technology and E-Governance involves:

- Database Administration

- Maintaining a functional and secure data network

- Communication Systems Administration

- Provide a resource for technical support

- Maintain consistent hardware & software purchasing, installation and licensing

- Improving overall system related work flow processes

| Section | Function |

|---|---|

|

Billing Section |

How Billing is done Billing is done using the Promun (ERP) package. The services are billed per property in the following categories: High density, Low Density, Institutions, Commerce and Industry Every Property (unit) has a unique account number assigned to it. Each service offered has a tariff/ charge assigned to it. Every tariff is identified in the system by a specific code. The different tariffs are configured to each account number in the system. After billing has been done, statements for each property are printed and distributed. (also account balances are sent through SMS’s) Once a month we raise charges for all the services except rates which are done quarterly |

|

Credit Control Section |

Debt Management, monitoring and collection through:

|

|

Payroll Section |

|

|

Insurance and Risk Management |

|

|

Stores |

|

Treasurer’s REPORT

BUDGET PERFORMANCE

Actual- The expenditure incurred during the current month

Budget- The amount allocated at the beginning of the period to be used/collected during the month.

VARIANCE-INCOME

Variance- the difference between the budgeted figure and the actual.

INCOME

Adverse – adverse its when the income collected is less than the budgeted figure

COLLECTED REVENUE < BUDGETED

Favourable -is when income collected exceeds the budgeted figure

COLLECTED REVENUE>BUDGETED

Structure of the Finance Department

The following are the major sources of revenue are those charged through the billing system:

- Rates

- Supplementary charges

- Rent

- Water

- Refuse removal

- Education levy

- Fire levy

- Sewerage

- Public lighting

Other sources of revenue are:

- Stand Sales

- Business Licences

- Plan Approval Fees

- Market fees

- Town Terminus fees

- Agreement of sale fees

- Clinic fees

- Ambulance fees

VARIANCE-EXPENDITURE

ADVERSE-This occurs when the actual expenditure exceeds the budgeted expenditure

ACTUAL>BUDGETED

FAVOURABLE-This occurs when the actual expenditure is less than the budgeted expenditure

ACTUAL<BUDGETED

CONSOLIDATED SUMMARY

EXPENDITURE Current- the expenses incurred during the current month.

Cumulative/year to date– is the total expenses incurred from the beginning of the budget period including the current month.

LIQUIDITY

DEFINITION: A measure of the extent to which an organization has cash to meet immediate and short-term obligations, or assets that can be quickly converted to do this.

In Accounting: The ability of current assets to meet current liabilities.

HOW DO WE MEASURE IT?

In our report liquidity position– is the difference between revenue debtors and revenue creditors.

CREDITORS/PAYABLES

DEFINITION: A party to whom money is owed by council

Age Analysis – is the grouping of creditors by the length of time their amounts have been outstanding (normally grouped as follows- current, 30days, 60 days, 90 days and 120 days and above

DEBTORS/RECEIVABLES

DEFINITION: Corporates and individuals who owe Council money for goods supplied and services rendered by Council.

Debit Raising-is the process of charging/billing of ratepayers’ accounts for water and services supplied to them for a particular period(usually one month)